By Robert Miller, NAOS Asset Management

The accepted wisdom in the Old World was that swans were always white. That was up until 1697, when Dutch explorer Willem de Vlamingh sailed up a river in Western Australia and spotted black swans gliding along its banks. Declaring something impossible is fraught with danger. One sighting was all it took to overturn a belief long held as a universal truth. As Nassim Taleb later put it in his now-famous 2007 book, The Black Swan, a single observation can “invalidate a general statement derived from millennia of confirmatory sightings of millions of white swans.”

It is from this story that Taleb coined the term we now use to describe events that share three characteristics — they are unpredictable, they carry a massive impact, and, after the fact, we concoct an explanation that makes them appear less random than they were. In other words, a Black Swan is the thing the collective did not see coming until it landed.

What Is a Black Swan, Really?

The most familiar recent example is COVID-19. The risk of a global pandemic — mandatory lockdowns, entire industries grinding to a halt — was not meaningfully reflected in valuations when equity markets were trading at near-record highs in late 2019. Then, within a matter of weeks, the S&P/ASX200 Index fell approximately 36% from peak to trough. Markets, by their very design, did not (and could not) price the risk in advance.

COVID is not alone. Other Black Swan events in recent memory include both the September 11 terrorist attacks of 2001 and the Fukushima nuclear disaster of 2011. In every case, the market’s collective expectation that these events would occur was effectively zero. This is only a mistake in hindsight…

“A mistake is not something to be determined after the fact, but in light of the information available until that point.” – Nassim Nicholas Taleb

In our view, this quote is one of the most important to internalise as an investor. It is far too easy in hindsight to look back at an investment decision and label it a mistake. The honest test is whether the decision was a poor one, given the information reasonably available at the time. Black Swans, by definition, fall outside that information set.

When a Black Swan Lands on a Single Company

While market-wide Black Swans are the ones which most suitably fit the definition above, equity investors are far more frequently confronted with company-specific Black Swan-type events. These are events that, ahead of time, were not on anyone’s radar, but which fundamentally alter the trajectory of a single business. These events are the types of things which can figuratively sideswipe investors, and in our experience, the share price reaction can be very severe.

One that comes to mind is an ASX-listed company we have followed for many years. Objectively, it is a strong business with a genuine competitive advantage, a credible management team and a very conservative balance sheet. Then, with very little warning, a one-off event occurred that materially reduced the share price in a short period. None of the standard risk frameworks would have caused the market to price in the possibility of such an event. It was a genuine Black Swan. This is the reality of investing in equity markets. No matter how thorough your research process, no matter how rigorous your pre-mortem, there will always be ‘unknown unknowns’ that you simply cannot underwrite in advance.

Volatility Is the Price of Admission

For equity investors, volatility is the name of the game. If you are not comfortable with severe drawdowns, then investing in equities is probably not for you. Crucially, volatility must be clearly distinguished from risk: the former is the degree to which a share price fluctuates, whereas the latter is the probability of a permanent capital loss. Volatility is the noise that surrounds the underlying value of a business — it has nothing to do with the business itself.

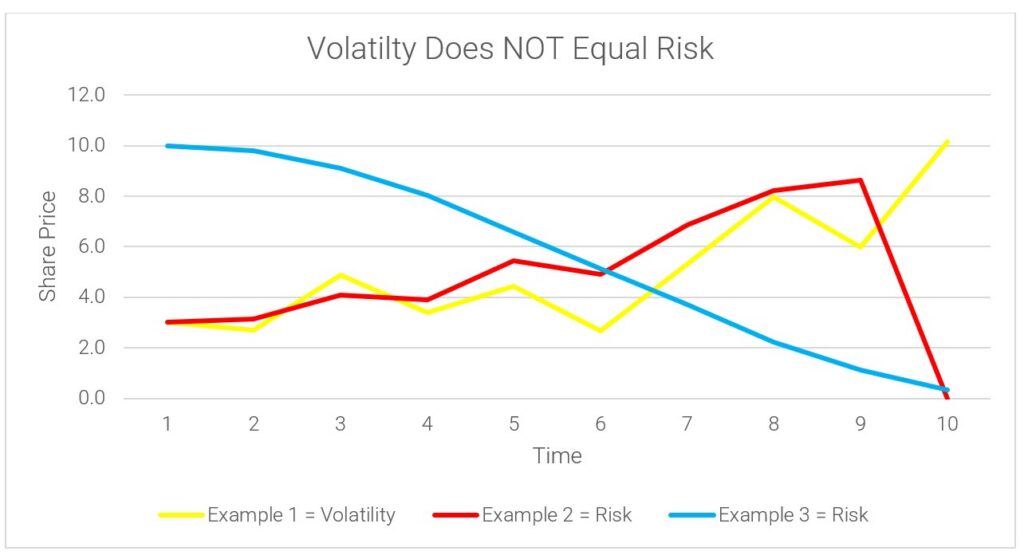

The graph below shows three theoretical examples of share price movement, example one, which demonstrates volatility and example two, which demonstrates risk. We can see that two of the scenarios result in significant capital loss over the period, despite lower volatility.

Source: NAOS

Example 1 (volatility) has the highest standard deviation (a measure of historical volatility), yet its share price has increased multiple times over the theoretical 10-year period. Conversely, Example 3 (risk) has a significantly lower standard deviation than Example 1, yet has resulted in a permanent capital loss event with the share price worth $0, as the table below shows:

| Example 1 = Volatility | Example 2 = Risk | Example 3 = Risk | |

| Standard Deviation | 52.8% | 42.7% | 22.1% |

“Volatility is our friend. Volatility has nothing to do with risk.” – Mohnish Pabrai

Even two of the highest-quality companies in the world, Microsoft Corp. (NDQ: MSFT) and Berkshire Hathaway Inc. (NYSE: BRK), have each suffered three share-price drawdowns of more than 50% in their listed histories. The world’s largest company, NVIDIA Corp (NDQ: NVDA), suffered an ~80% drawdown during the GFC. Closer to home, BHP Group Ltd (ASX: BHP) and Rio Tinto Ltd (ASX: RIO) have each experienced three >50% drawdowns, albeit they are far more cyclical in nature than MSFT and BRK. Some of the largest, most defensible, best-managed businesses on the planet have each been cut in half on three separate occasions. Black Swans, real or perceived, are a feature of equity markets — not a bug.

The Three Choices in a Black Swan

When a Black Swan event hits, whether it’s a market-wide occurrence or an isolated company event, as investors, we are faced with three choices to make. They are:

- Sell – Liquidate an investment on the basis that the facts have fundamentally changed. The honest follow-up question is, am I getting caught up in the crowd and selling at the bottom?

- Hold – Wait to see how the situation evolves before making a decision. Often the best answer in equity markets is to do nothing (but not always). This approach requires an element of emotional discipline.

- Buy – Both upside and downside overreactions in equity markets are commonplace. Has an investment become genuinely mispriced, and is the risk profile lower given the compensation of a lower share price justifies this?

There is no formula for which choice is correct. But in our experience, perhaps the most important question an investor can ask themselves in the wake of a Black Swan event is this:

Has [insert Black Swan event here] fundamentally changed my long-term thesis for owning this investment, or has it rather created a period of short-term volatility? If I didn’t own it today, and the market was about to close for five years, would I still want to buy it?

If the answer to the second question is yes, then panic selling at the bottom is almost certainly the wrong response. If the answer is no, then your thesis has been broken and selling, even at a loss, may be the right call.

Building Systems That Handle Volatility

One of Nassim Taleb’s most enduring contributions, beyond simply identifying the Black Swan phenomenon, is the framework he developed in his follow-up book Antifragile. His central argument is that, rather than trying to predict and eliminate every conceivable source of randomness (an impossible task), investors should build systems and portfolios that can withstand volatility and ideally benefit from it. This is a subtle but profound shift in mindset. You stop trying to forecast the next Black Swan and start preparing for the inevitability that one will arrive at some point.

“The biggest risk is always whatever no one is talking about, because if no one’s talking about it they’re not prepared for it.” – Morgan Housel

The NAOS Perspective

You cannot control what you cannot control. Black Swans, by their very nature, are unforecastable. You would need to be Superman to say the opposite. What you can control is the quality of the businesses you choose to own when the unexpected arrives.

At NAOS, our view is that investing in companies that exhibit the following characteristics gives you the best chance of weathering a Black Swan and, more importantly, in the event of a market-wide Black Swan event, being one of the first to get back up when everyone else has fallen flat on their face:

- Sustainable business models that don’t depend on benign macro conditions and can lay claim to having pricing power;

- Resilient balance sheets, with minimal-to-no debt;

- Management teams with proven track records, deep alignment, and credibility;

- Operating in industries with genuine long-term structural tailwinds; and

- A genuine competitive advantage that is difficult for competitors to replicate

Companies that carry large debt balances, weak operating models, and stretched balance sheets are, in our experience, far less likely to recover after the music stops and before it starts back up again.

We will never be able to eliminate Black Swans from our investment lives, nor should we try. However, by focusing on what we can control, the quality of the underlying companies we own, we give ourselves the best possible chance of not just surviving the next one but thriving on the other side of it.

The late Charlie Munger had a mental model to always invert the problem or question at hand. With that being said, perhaps we should not be thinking about how to avoid the Black Swan; rather, we should be thinking about how to make sure we can keep walking when one shows up.

Important Information: This material has been prepared by NAOS Asset Management Limited (ABN 23 107 624 126, AFSL 273529) and is provided for general information purposes only and must not be construed as investment advice. It does not take into account the investment objectives, financial situation or needs of any particular investor. Before making an investment decision, investors should consider obtaining professional investment advice that is tailored to their specific circumstances.

(25)")