")

By Shani Jayamanne, Senior Investment Specialist, Morningstar

8 March 2024

The media has recently been filled with commentary on the gender pay gap. We constantly hear about differences in retirement savings between men and women. The solution seems clear – close the pay and retirement savings gap and we will reach equality.

I support these efforts. Yet my own exploration of retirement outcomes makes something abundantly clear. Women don’t need the same levels of retirement savings as men. Women need more than men to support the same retirement outcomes.

According to the Australian Institute of Health and Welfare, women experience distinctly different health outcomes to men. Their life expectancy is longer, but their ‘total disease burden’ is also higher as women are more likely to live with a chronic disease than die early from a disease. Half of all Australian women have one or more chronic conditions that likely require ongoing support and specialist care.

A longer retirement with a higher likelihood of specialist care leads to far different retirement outcomes for women. Planning and funding retirement should take these differences into account.

Lower retirement savings with higher costs of care

Compounding these challenges are the lower levels of retirement savings for women. There are two main drivers. The first is the gender pay gap. Earning less than our male counterparts over decades has a significant impact on our superannuation, with lower contributions meaning lower investment balances to compound and grow.

For example, the median female earnings in August 2023 was $1,150, contrasted with $1,500 for male. A caveat to this is that a higher proportion of females work in a part time capacity. Nevertheless – this still impacts superannuation balances.

If we take the average female balance (source: AustralianSuper) of $30,033 at 25 and project the retirement balance out to 67 with the median weekly salary, the result will be $327,661*. For males, the same model results in $415,351.

I encourage everyone to project future levels of retirement savings by using the MoneySmart calculator for Retirement savings. Understanding future outcomes early provides the opportunity to course correct before it is too late.

Contributors to the total disease burden

Eliminating the gender gap in retirement savings is an admirable goal. It is something that I fully support but it may not be enough. We need higher levels of savings to account for higher healthcare costs and longer life expectancy.

Although these situations are mostly unavoidable financially, they can be minimised by investing early and adequately planning for likely outcomes.

Exact future healthcare costs are hard to define. This is why planning is crucial. The planning must take into account the disparity in women’s wages, life expectancy, career breaks, current superannuation balances and likely health outcomes. The culmination of these factors will often multiply in the form of lost investment earnings, and a lower quality of life in retirement, when most of these health issues occur. We need to utilise the lower tax rates of superannuation to invest and self-insure for our future selves.

Research from the National Centre for Epidemiology and Population health shows that ‘individuals with multiple chronic illnesses can spend up to six times the amount spent by those without a chronic illness. Those on lower incomes are fifteen times more likely than those on higher incomes to incur catastrophic health care costs (>10% of household income).’

Another study from the University of Technology Sydney surveyed 800 women with osteoarthritis. The study showed that on average, these women aged between 53 and 94 had more than seven specialist care appointments in one year – for a single condition. After Medicare rebates, $673 was required to cover the appointments, therapies and medication.

There’s over one million Australians that have multiple chronic conditions that can be a heavier financial burden. The Grattan Institute found that they pay more than $1,000 each year on out-of-pocket expenses. The same study found that over the past decade, out of pocket costs have increased by 50%.

Some chronic illnesses are more expensive than others. For example, Alzheimer’s would require full time care for developed cases.

How to account for health costs in retirement savings

Start with understanding your expenses in retirement

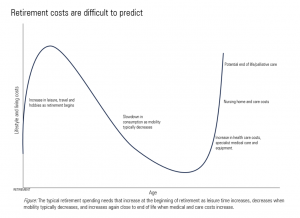

The general rule is that expenses increase at the beginning of retirement as many retirees decide to travel and pick up hobbies. These costs tend to decrease after time, and then surge due to specialist and end of life care. However, there may be significant reductions in spending, such as if you are making a sea change, or if you’ve paid off your mortgage.

As retirement progresses, this is where you may need to consider more costs going towards chronic conditions. You may also need professional care. Like retirement in general, the duration and extent of care is difficult to predict. However, the whole point of planning is to address potential contingencies.

A baseline for retirement planning is your current salary and continuing your current lifestyle in retirement. Then adjustments can be made. Your expenses may differ from your pre-retirement salary for several reasons. The first is that there will be less incidentals that are associated with work. For example, transport to and from work and lunches that you may buy most days. However, you will have free time in retirement that could mean increased leisure costs and travel costs. This will depend upon how you envision retirement and what it is achievable with your retirement savings.

ASFA’s Retirement Standard Detailed Budget Breakdown outlines that the average costs per year to cover medical and health related costs in retirement is $5,880 for a single person and $11,018 for a couple.

This of course, is a general guideline. It is difficult to know how much to exactly put aside as the future is unknowable. However, having a goal instead of simply trying to maximise your wealth will allow you to manage the risk in your portfolio and increase the likelihood that you will achieve your retirement goals.

Now that you have a general guideline of expenses, you can use this to understand how much you need in retirement. This article I have written goes through the steps of finding out how much you need to retire and explores resources to create a plan towards this goal.

Other factors that will impact your retirement savings

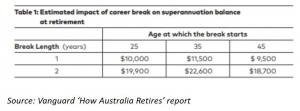

Career breaks are another driver of lower levels of retirement savings with women disproportionally impacted.

Around 40% of working age Australians expect to take an extended break from work, and 1 in 2 under 35 expect to take parental leave.

Career breaks can come in all shapes and sizes. A break can be used to care for elderly family members, as parental leave, for extended travel or for study. Regardless of the reason, it means that your superannuation contributions will stop. The exception to this is parental leave, where there’s government mandated contributions from your employer.

Government mandated parental leave contributions may not be adequate. Many women take a longer period off work to care for new children (an average of 32 weeks leave) than the mandated parental leave benefits (18 weeks of leave).

The issue with career breaks, especially earlier in life, is that your contributions have less time to compound. The impact of longer career breaks is significant for superannuation balances.

Extra contributions prior, during or after the career break

For career breaks that are planned or unplanned, extra contributions in the lead up, or upon your return to work, can ensure that you do not end up with lower retirement outcomes.

This can be done in a few ways. Planned career breaks are relatively straightforward – it is important that you financially plan for these breaks. A plan will enable you to replace the contributions that you will miss during your break.

Unplanned breaks are a little more difficult. These breaks mean that you will often be dipping into savings or emergency funds to support yourself and will not have the resources to also contribute to your retirement.

According to the Australian Financial Security Authority, the government agency for those in financial hardship, on average, women have a 42 per cent lower superannuation balance at retirement than men. However, this gap is likely a drastic underestimate as most 60-year-old men and women would have only had superannuation as we know it for a portion of their life. Assuming you start work at 22 years old and retire at 60 with 8 per cent annual returns, a woman would need to save an additional $513 a year to close this gap. A good tool to use is the MoneySmart Superannuation Optimiser. It will allow you to see the impact of any voluntary contributions and the tax concessions received. Regardless of career breaks, it gives you a general idea of how to optimise your contributions into super while taking your take home pay into account.

Spouse co-contributions

If you have a spouse, there are ways that they can contribute to your super. The first is contribution splitting. Contribution splitting allows you to split the super contributions that have been made. This can include up to 85% of the contributions in that financial year.

Changing asset allocation

If you have a while left until retirement, you’re able to take on a more aggressive asset allocation to account for missed contributions. When we invest, we are exchanging risk for return. Different asset classes (shares, bonds, cash etc.) have different risk and return profiles. Cash has low risk, and a relatively lower return than other asset classes over the long term. Shares have a higher risk, and expectation for a higher return.

In 2017, Fidelity conducted a study on nearly 8 million account holders. The study found two revealing differences in the saving and investing habits of men and women. The first is that women save more than men. Women saved an annual average of 9 per cent of their pay compared to an average of 8.6 per cent for men. Not only did they save more, but women also made better investors. Women outperformed men by 40 basis points, or 0.4 per cent. This seemingly small difference in savings rates and investment returns can make a big difference over the long term.

Changing the types of assets you are invested in in your superannuation will have a significant impact on your retirement savings.

We talk about this in detail in our Investing Compass podcast episode on Portfolio Reviews.

This article has been prepared by Morningstar Australasia Pty Ltd (AFSL: 240892). The information is general in nature and does not consider the financial situation of any individual. For more information refer to our Financial Services Guide at www.morningstar.com.au/s/fsg.pdf . You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement before making any decision to invest. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser.

*The assumptions for this model is 7% p.a. investment returns, $74 in admin fees and 0.5% in investment fees. It is assumed there are no pay rises.

(25)")