By TAMIM Asset Management

17 April 2022

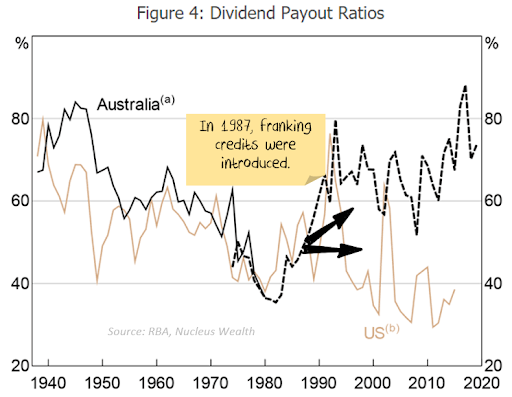

Dividend investing is as Australian as Vegemite, Tim Tams,…or maybe pavlova? The ASX has a higher dividend yield than most other share markets around the world, in large part due to the dividend imputation system (commonly called franking). Introduced in 1987, the imputation system gives shareholders a tax credit with their dividend for the tax already paid on these profits by the company.

In Australia, company profits are usually taxed at 30%, so investors who receive fully franked dividends generally only need to pay tax on the difference between 30% and their marginal tax rate for the dividends they receive. Imputation systems are generally rare and the U.S. doesn’t have one, but New Zealand and several other markets do.

Dividend Payout Ratios in Australia and the United States of America

Why Pay More?

According to investing theory, there are a few different reasons why companies pay large dividends. Three of the most significant are “signalling,” “bird in the hand” and “agency theory.” Signalling refers to the fact that managers and members of the Board of Directors have more information about the company than outside investors. By changing the size of the dividend, insiders can convey information about how well the firm is doing (with increases signifying the company is doing well and cash flows are likely to increase in the future, and vice versa). This is particularly relevant for business models that are more specialised or opaque (difficult for investors to judge from the outside), such as pharmaceuticals or advanced technologies.

“Bird in the hand” refers to how investors would prefer to receive cash today, because of the uncertainty of greater dividends (or capital gains) in the future. Investing is not a hard science and the future is difficult to predict, particularly in a capitalist and often highly competitive environment. If investors are confident about a company’s future prospects, they can always use the dividend to buy more shares!

Agency theory focuses on the separation between the owners of the company (investors) and the management team. The main concern here is that if the cash is retained inside the company, managers may “waste it.” This often shows up as big acquisitions, as managers try to build their empire and increase their own remuneration. The media industry is notorious for this (News Corp’s (ASX: NWS) acquisitions of MySpace, Amplify and The Wall Street Journal spring to mind), and it can also be a bigger risk in highly cyclical industries such as oil, gas, mining and resources (when companies can become flush with cash at the top of the cycle and believe the good times will last forever).

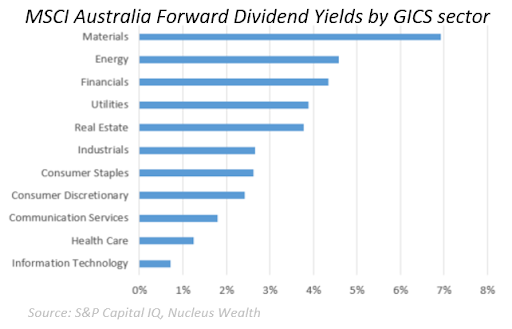

MSCI Australia Forward Dividend Yields by GICS Sector

In practice, there are a few more reasons for a high payout ratio (the proportion of profits paid out as dividends). Certain shareholders prefer current income (particularly retirees, including the “SMSF army”) and there are specific groups of shareholders that have low tax rates (some even receive refunds from the franking credits) or are prohibited from spending the shares’ principal (e.g., trusts and endowments).

There are also businesses that can pay out the majority of their profits because they do not require much extra capital to grow (funds management, for example) or they have a negative working capital cycle and actually generate cash as they grow (which we discussed in one of our previous articles Which Quality Stocks Can Survive a Downturn?). There are also businesses that are in structural decline, and investors would prefer to have their money taken out of these businesses to redeploy into better future opportunities. Cigarette companies are a good example today: traditional cigarette consumption is declining and producers listed on the share markets typically pay out a high proportion of earnings.

Finally, the majority of businesses do not have sufficient growth opportunities (companies on the share market are by their nature larger and more mature). This might be because growing too fast in their respective industries is risky (writing a huge number of bank loans or insurance policies to new customers for instance), or because they have “saturated” or taken a substantial portion of their markets (Woolworths and Coles, for example).

Get Low and Prosper

With all these pros, what are the arguments against having a big dividend? Tax implications are the most obvious one. Unless the franking credits entirely cover the tax expense, dividends have an immediate tax liability–unlike capital gains, where the tax impact is deferred until the investor realises the gain (i.e., sells the investment). While it might not seem like much on any individual investment, paying this tax at a later date can have a serious impact on compounding your wealth.

Another key reason is to avoid cutting the dividend and allowing it to grow over time. Reducing or eliminating the dividend can have a dramatic impact on the share price, which far outweighs any benefit an investor will receive from the dividend itself (as an example, Hanesbrands (NYSE: HBI) fell ~28% at the start of February when it suspended its dividend). That’s why companies typically have long-run target dividend payout ratios that are based on long-run sustainable earnings (not short-run changes in earnings).

Maintaining a low payout ratio can also provide a buffer against the challenging ups and downs of the business world, while allowing the company to continually pay dividends each year. Take Sydney Airport during 2020 for example. While it’s true this was a highly abnormal year and the company was unusually impacted, its dividend policy of paying out essentially all available cash flow combined with a very high level of debt meant that any major disruption to the company’s operations would cause a cut or suspension in the dividend.

The fourth (and often most important) reason relates to the company’s growth prospects. Companies that are growing their revenues and profits are able to grow their dividends more easily and sustainably over time. If the payout ratio is too high, this growth then has to be funded via debt (which can only be done to a certain level) or issuing new shares (which dilutes your shareholding, particularly if it occurs at a low share price). If the growth of the business is limited by not having enough capital (because the dividend is too high), it can quickly stagnate and start shrinking–imperiling the existing dividend.

In fact, a high dividend yield can often be a sign of a business under extreme pressure, where the dividend has not yet been “reset.” Look no further than the ASX’s highest-yielding stock in March, Magellan Financial Group (ASX: MFG). With rapidly declining assets under management, it seems almost certain that the trailing yield of 13.87% is not likely to be repeated.

Everything in Moderation

Dividends are an important contributor to an investor’s long-term returns. They also provide cash flow, convey information to outsiders, and reduce agency costs. In fact, a number of long-term share market successes highlight the importance of dividends in instilling discipline in the management team. Both Admiral (LSE: ADM) and Dicker Data (ASX: DDR) have a residual dividend policy (they pay out all the cash flow not needed to run or grow the business each year) that strengthens their annual planning processes.

However, there can be “too much of a good thing.” Having a payout ratio that is too high can deprive the company of funds it needs to maintain its competitive position and to invest for future growth. This can cause the company to cut or suspend its dividend during any operational challenges and limits the ability of the company (and the dividend) to grow over time. A high dividend yield can also be an indicator of a declining business, where the prior dividend simply isn’t sustainable.

Investors looking for dividend-paying shares might instead look to those companies with moderate payout ratios and steady growth rates, such as ASX stalwart Brickworks (ASX: BKW), which typically pays out around 50% of its sustainable earnings. Companies that have historically paid special dividends are also a good hunting ground for outperforming stocks–particularly prior to any government tax changes (note: investment powerhouse Washington H. Soul Pattinson (ASX: SOL) paid a special dividend in December). It’s also worth remembering that while it might be psychologically more difficult, selling some shares to create your own dividend produces the same result – only more tax efficient.

(25)")